Invest in Floor & Decor Stock and Watch on Your Portfolio for Floor-ish

Summary

Floor & Decor, founded in 2000, is a multi-channel specialty retailer and commercial flooring distributor with 160 warehouse-format storefronts and two small design studios in 33 states.

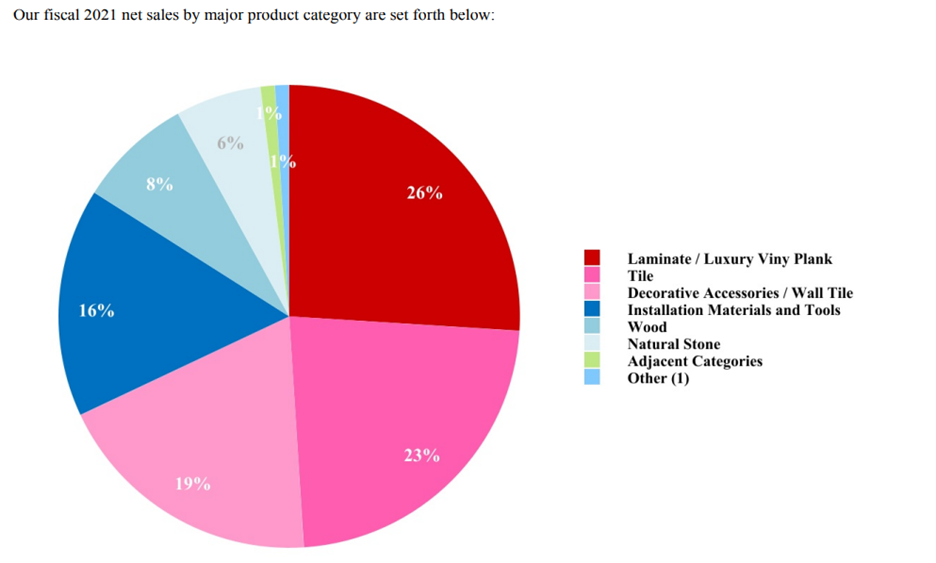

The company targets professional installers, commercial businesses, and Do It Yourself customers who buy products for professional installation, with a wide selection of in-stock tile, wood, laminate, vinyl, and natural stone flooring, as well as decorative and installation accessories.

The warehouse-format locations of Floor & Decor, which average 78,000 square feet, are larger than many specialized retail flooring competitors and provide a wide selection of hard surface flooring alternatives and accessories.

FloorandDecor.com, the company's website, shows items, provides design ideas and educational resources, and allows consumers to purchase things for in-store pickup or delivery.

Due to its distinct value offering and customer loyalty within its target market categories, Floor & Decor has continuously experienced significant comparable store sales growth, averaging 12.6% over the last five years. Floor & Decor plans to establish at least 500 locations around the country during the next 8-10 years.

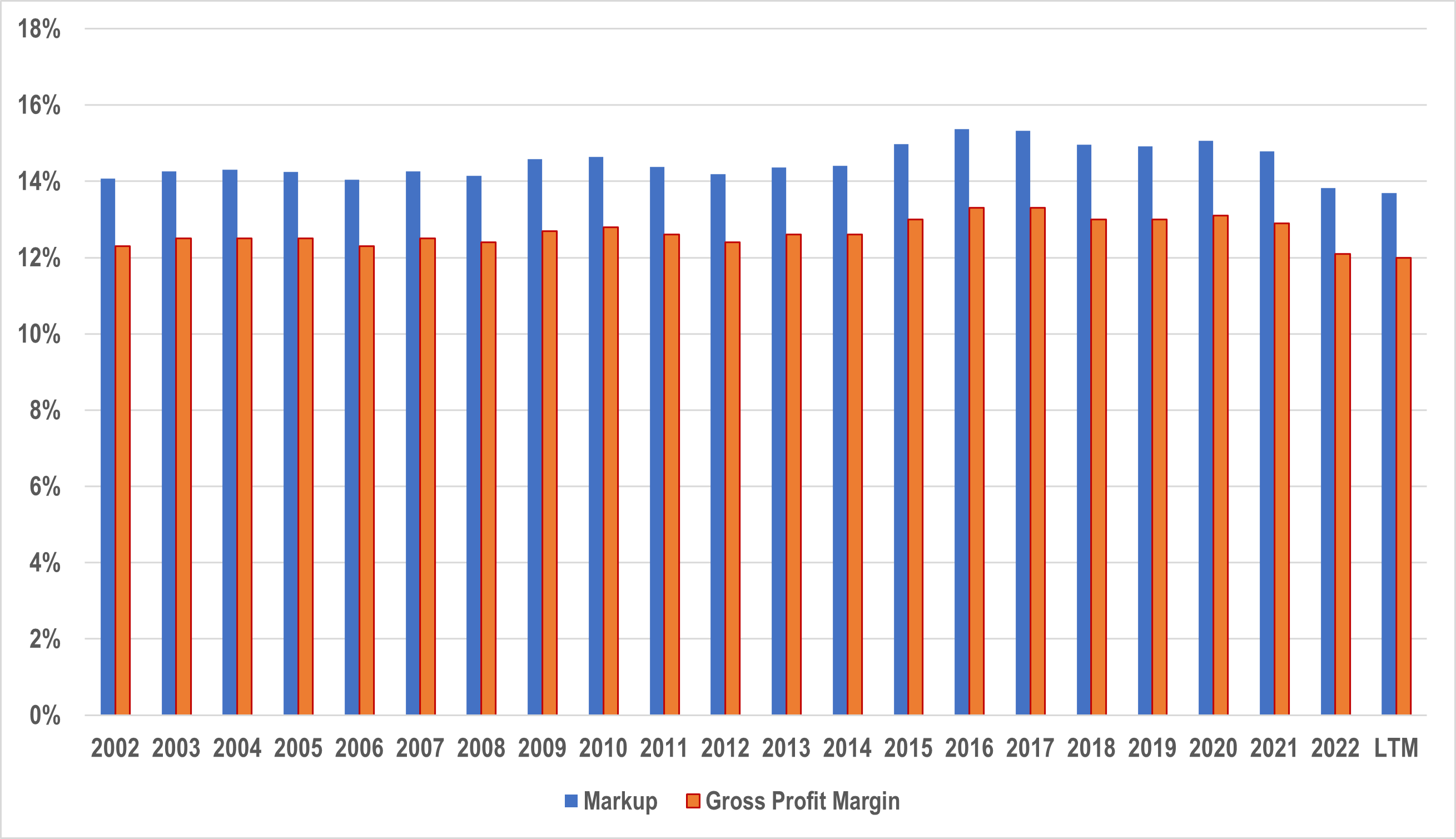

Costco is a bargain-hunters paradise, with its everyday low pricing (EDLP) strategy of marking up products by a maximum of 14% over cost and reputation for low prices. But it's not just about the discounts - Costco's low operating costs and measured approach to growth have also contributed to its success, according to Nick Sleep of the Nomad Investment Partnership. And other companies have taken notice, with Floor & Decor Holdings following in Costco's footsteps by offering a wide selection of products at low prices and purchasing directly from manufacturers who can offer the best value proposition to customers. As Mohnish Pabrai wisely stated, "You don't need to create your own ideas – you can clone them." Floor & Decor Holdings has taken this advice to heart and is reaping the rewards.

Overall, it is apparent that companies such as Costco and Floor & Decor Holdings have achieved success by providing customers with low prices and a diverse product variety while simultaneously concentrating on efficiency and sustainability. Furthermore, their strategy of purchasing directly from manufacturers to ensure competitive pricing is critical to their business model. We'll take a deeper look at Floor & Decor in the next section to see how they're "Taking the Flooring World by Storm One Step at a Time" with their extensive choice of goods and services for professional installers, do-it-yourself clients and homeowners alike.

Floor & Decor: Taking the Flooring World by Storm One Step at a Time

If you're in the market for new hard surface flooring, you'll want to check out Floor & Decor, a company that has been providing a wide range of products and services to professional installers, do-it-yourself customers, and homeowners since its founding in 2000. Led by Vincent West, an experienced entrepreneur with a background in retail and real estate, Floor & Decor operates 160 warehouse-format stores and two small design studios across 33 states.

With its broad selection of in-stock tile, wood, laminate, vinyl, and natural stone flooring, as well as decorative and installation accessories and adjacent categories, this multi-channel specialty retailer and commercial flooring distributor is a one-stop destination for all your flooring needs. Whether you're a professional installer, a DIY enthusiast, or a homeowner looking for professional installation, Floor & Decor has something for everyone. Don't waste any more time and energy on the daunting process of finding the perfect flooring – let Floor & Decor make it easy for you.

Aside from unsolicited advertising (full disclosure: I own no common stock in Floor & Decor), the question on everyone's mind is how sustainable their business model is and how the company earns money. As we go deeper into the world of Floor & Decor, it becomes evident that the company's strategy of delivering a diverse range of items at affordable rates, sourcing directly from manufacturers, and emphasizing efficiency and sustainability has proven to be a winning recipe. But don't just take my word for it; let's have a look for ourselves and discover how Floor & Decor is shaking up the flooring market while generating a profit one step at a time.

Looking at a company's customer base and seeing how it drives revenue is always interesting. Floor & Decor appeals to a varied set of clients, including professional installers and commercial enterprises (referred to as "Pro"), Do-It-Yourself enthusiasts ("DIY"), and homeowners who purchase materials for professional installation ("Buy it Yourself" or "BIY").

The client base of Floor & Decor is essential to the company's success. With a diverse clientele, the firm benefits from loyal Pro clients and homeowners representing a sizable market for the brand. The company's Pro customers are "loyal, make regular purchases, and help promote their brand." This is advantageous for Floor & Decor since repeat clients are a significant source of revenue for any business. Furthermore, homeowners make up a sizable section of the BIY clients, which is not unexpected given that they will most likely want new flooring at some time.

In recent years, Floor & Decor has been on a roll, with overall sales growth that would make even the most seasoned Wall Street veteran green with envy. The firm has grown at a compound annual growth rate of roughly 23.5% during the last decade. But what is the source of this success? The company's ability to traverse the frequently stormy seas of the retail and commercial sectors holds the key.

According to the company's economic research, Floor & Decor sales are impacted by general economic factors such as consumer spending and housing market conditions. This is due, in part, to the company's sensitivity to several factors that influence consumer purchasing, such as disposable income, unemployment patterns, stock market performance, consumer debt levels, credit availability, and general consumer confidence in the economy. However, unlike many businesses thrown around by the whims of the market, Floor & Decor has shown to be versatile and nimble, able to remain ahead of the curve and continue to develop even during economic downturns. Floor & Decor can foresee changes in the economic landscape and respond accordingly if they have a strong awareness of these aspects in specific regions they serve.

Of course, knowledge of the local economies they serve is only one component of the puzzle. The business model of Floor and Decor is also crucial to its success. Net sales include in-store and e-commerce transactions; revenue is recorded when the firm meets its customer contractual performance commitments. When the consumer takes possession of the inventory, the company's performance requirements for retail store sales and orders submitted through its website are met. This enables the company to serve a diverse set of online and in-store customers.

Floor and Decor are quickly rising to prominence in the retail and commercial sectors. The firm is well-positioned for sustained development and success with a sound business plan, agility, and a good grasp of the environment. The company's success is shown in its highest YoY growth rate of 41.5% in 2021, demonstrating its capacity to adapt and survive in a continually changing economic climate. And it's simple to see why with figures like these.

Floor & Decor has effectively maintained and expanded sales at its existing stores, as seen by its reasonably consistent Same Store Sales Growth, as shown in the table. This clearly implies the company's realistic plans and processes for maintaining present sites. On the other hand, the company's New Store Sales Growth has been more variable, with a combination of success and failure in new store openings. However, the total growth % remains positive, indicating the company's effectiveness in extending its operations.

Blockbuster is a historical example of a firm that tried to grow too quickly and lost sight of its fundamental business. Blockbuster's narrative is akin to attempting to construct a house of cards in a cyclone; they expanded too rapidly, opening hundreds of locations, but were unable to adjust to changing circumstances, and BAM! they were out of business. Blockbuster's failure to focus on its core business and adapt to the digital revolution ultimately led to its demise, proving that "out with the VHS cassettes, in with the streaming" was correct. The story's lesson is that while it is necessary to grow, it is also critical to maintain a firm’s foundation.

After considering how they make revenue, Floor & Decor must consider how they spend that money to preserve or expand the business's economic moat. Understanding and controlling their operational leverage is one method to do this. The amount by which a company's revenue and profits shift in reaction to a change in its operating expenses is measured as operational leverage. In layman's words, it's a lever that the corporation may use to adjust how much their earnings vary when their expenses fluctuate.

Let's use the example of a mobile app development business to grasp this concept further. The owner of this firm discovered that they had an operational leverage of 2. This meant that every 1% rise in operating costs reduced the company's sales and earnings by 2%. As a result, if the company's operational expenditures rose by 10%, sales and profits would fall by 20%. However, if the firm could reduce its operating expenses by 10%, its sales and earnings would rise by 20%.

The owner of the mobile app development firm was now aware of this link and realized that by controlling their operating costs, they could use the operational leverage lever to boost their profitability. They set out to identify ways to reduce operational expenses while preserving the quality of their mobile apps. As a consequence, they were able to improve earnings and retain the business's economic moat.

Even though Floor & Decor is in the flooring business rather than app development, the economics of operational leverage remain the same. According to the data above, selling and store running expenditures have been 80% of total operating expenses over the previous decade, which has been relatively stable. During this time, sales expanded by +25%, while operating margins increased from 7% to 9% (a 2% CAGR), with pre-tax operating profits rising from 21 million to 339 million, a 30% CAGR in 11 years. Meanwhile, the company's selling and store operating costs grew by 27%. This rise in earnings was caused by higher spending on SG&A and capital expenditures that had positive economic value.

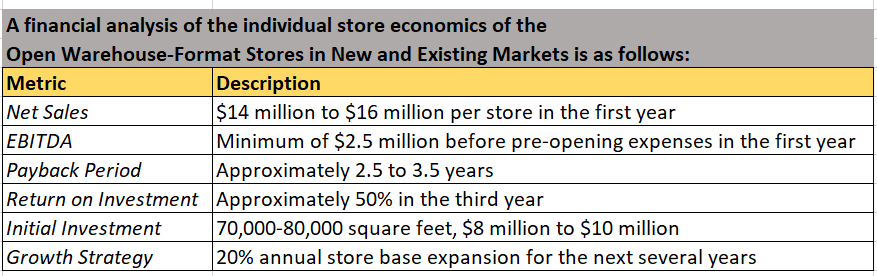

The company plans to expand its store base to at least 500 over the next 8 to 10 years, targeting new openings in both new and existing adjacent and underserved markets. The company's new store model is designed to deliver strong financial results and returns on investment. The company has built a strong team of employees to support its store-level success. Each of their stores is led by a CEM (Customer Experience Manager) and is supported by an operations manager, product category department managers, a design team, a Pro sales and support team, and several additional associates. Outside their stores, they have employees dedicated to corporate, store support, infrastructure, e-commerce, call center, and similar functions, as well as support for their distribution centers and sourcing office.

The new model targets a size of 70,000-80,000 square feet, with a total initial net cash investment of approximately $8 million to $10 million. The company targets net sales on average of $14 million to $16 million per store in the first year. Additionally, the company targets a minimum of $2.5 million in four-wall adjusted EBITDA before pre-opening expenses in the first year. This indicates that the stores are expected to generate a positive cash flow from operations in the first year. The company expects a pre-tax payback period of approximately two and a half to three years, with cash-on-cash returns of roughly 50% in the third year.

The company's growth strategy is ambitious, intending to grow its store base by approximately 20% annually for the next several years. This is supported by the company's performance of new stores opened over the last three years, the performance of older stores over that same time frame, disciplined real estate strategy, and the management team's track record in successfully opening retail stores. The key details are provided in a table.

A financial analyst's evaluation of a company's development potential and future economic effect is critical. Regarding year-over-year sales growth, most experts predict a 15% increase in 2023 and an 18% average growth rate from 2024 to 2026. Based on the company's current sales of 4 billion in the past year, this would boost revenues to 4.8 billion in 2023 and 8 billion in 2024, with operating margins of 9.1% to 9.9%. In the following years, this would result in an EBIT of $500 million to $700 million.

However, the company's development ambitions, which include adding 500 warehouse shops, may result in low free cash flow in the short term, thus limiting the cash accessible to equity investors over the next 5 to 8 years. This might induce short-term investors to sell their shares, lowering the fair value.

On the other hand, if the business successfully executes its expansion and continues to increase same-store sales at its current pace or even 200 to 300 basis points lower, the firm's actual economic worth would be considerably more significant than its current market price reflects. When assessing the company's prospective worth, investors must examine the short-term effect of the firm's expansion and the long-term potential for growth.

In conclusion, by executing a business strategy that stresses cheap costs, diversified product options, and efficiency, Floor & Decor has shown to be a vital participant in the flooring sector. The company's focus on purchasing directly from manufacturers and keeping solid client relationships has resulted in long-term growth and profitability. While the stock analysis makes a solid argument for investing in Floor & Decor, the individual investor must undertake more research and make their own educated choice. "The floor is yours," as the expression goes.